Explainer – How do bonds work?

Unlike shares, bonds are not usually the flashy upstarts of the investment world, with every move reported in the media. […]

Unlike shares, bonds are not usually the flashy upstarts of the investment world, with every move reported in the media. […]

As parents, one of the most valuable legacies you can leave your children is the gift of financial literacy. Providing

I’ve been a financial adviser for about twenty years now. I still get a ‘buzz’ out of making a positive

Just over 10 years ago we were in the midst of what is now known as the Global Financial Crisis

Generally speaking, there are two ways to make more money in life: by working day in, day out, or by

For many of us, we are able to contribute to superannuation for our entire working lives. Thanks to the superannuation

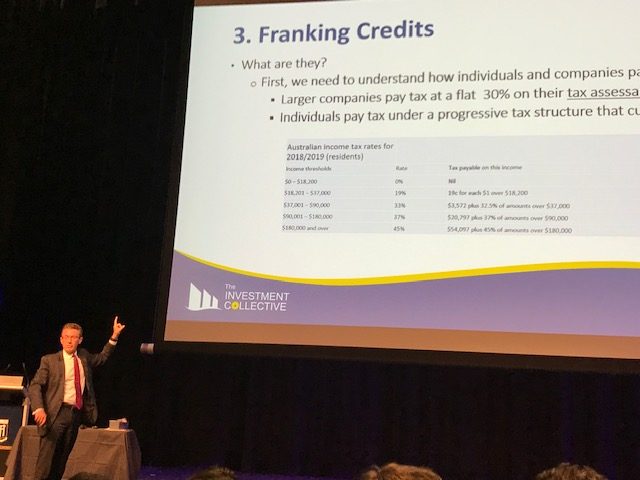

During our lifetime we all pay tax on our income at some point. This is called Pay As You Go

The word mortgage originated in England during the middle ages from the old French “death pledge.” This pledge refers to

Health Insurance, it’s a divisive subject. Some people swear by it, others refuse to even consider it. The reality is,

Life insurance has a special part to play at various points in your life. But first, what is life insurance?