Small businesses are vital to our economy and their sale can help fulfil their owners’ retirement dreams. Since September 1999, there have been a number of Small Business Capital Gains Tax (CGT) Concessions available to allow business owners to cash in on years of hard work, blood, sweat and tears. However, it is important that these concessions are correctly navigated; otherwise, there is a good chance that the “Taxman” will walk away with a big chunk of your hard work.

Business and Active Assets

The CGT provisions give a number of concessions to clients who sell a business or active business assets. An active asset is:

- an asset the taxpayer owns and uses or holds ready for use in carrying on a business and has been active for the lessor of 7.5 years or 50 percent of its life;

- an intangible asset inherently connected with the business (e.g. goodwill); or

- an interest or shares in a resident company or trust where the market value of the underlying active asset is up to 80 percent of total assets for at least half of the ownership period of the interest/shares.

Eligibility

To be eligible for the concessions the following conditions must be met:

- you are an individual, partnership, company or trust;

- you are carrying on a business;

- you are a small business, defined as having an aggregate annual turnover of less than $2 million; and

- your net assets value plus the net asset value of the client’s associates must be less than $6 million (excluding home, personal use assets, life policies and superannuation.

The Concessions

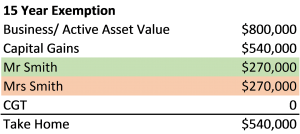

15-year Exemption

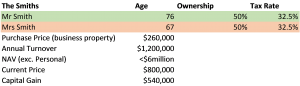

If the business or active asset was owned continuously for 15 years, and you are over age 55 and retiring, you can sell the asset or business without being assessed for capital gains. In our example above, the Smiths would be able to take home $270,000 each.

50% Active Asset Reduction

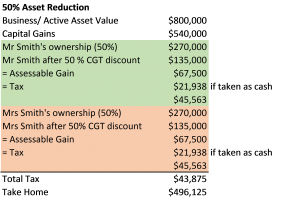

There is a 50 percent reduction on the capital gain from the sale of an active asset or business. This is in addition to the 50 percent CGT discount if the asset has been held for 12 months or more. If Mr and Mrs Smith implement this strategy they would incur a $43,875 tax bill and take home $496,125.

Retirement Exemption

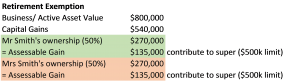

A client can elect to have a capital gain of up to $500,000 from the sale of an active asset or business treated as a superannuation benefit payment. If you are under 55, then this amount must be contributed into a superannuation fund and will add to the tax-free component. Once you reach the age of 60, all superannuation benefits are exempt from the tax, provided you meet the conditions of release. This strategy can be applied after the CGT discount and would allow the Smiths to contribute $135,000 to each of their superannuation accounts.

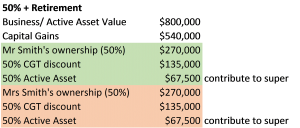

50 percent Asset Reduction + Retirement Exemption

If you have multiple business assets that you wish to sell to fund your retirement, you may be at risk of exceeding the $500,000 limit. To circumvent this limitation, it is possible to apply the 50 percent asset reduction as well as the Retirement Exemption. This strategy allows the Smiths to contribute $67,500 to each of their superannuation accounts, providing breathing room for an additional contribution of $432,500 to each down the track.

Rollover

If you sell an active asset, you can defer all or part of the capital gain for two years. You can defer this even longer if you utilise the proceeds to acquire a replacement asset, or if you spend money to improve an existing asset. This concession can also be applied after the 50 percent asset reduction.

It is vital that your personal financial position is carefully analysed when considering these concessions, as the above is provided as general advice only and should not be taken to be personal advice. Even if your circumstances are similar one of the above examples, please speak contact us to a business consultant today.

The last thing you want is to see the proceeds of your hard work end up at the ATO when you had access to professionals that could have navigated you through this tricky process. So if you are a small business owner with an eye on retirement, please come in to see one of our helpful Consultants or Financial Advisers to get a plan specifically tailored to your financial goals and objectives.