For many of us, we are able to contribute to superannuation for our entire working lives. Thanks to the superannuation guarantee arrangement, employers are obliged to contribute a minimum percentage (currently 9.5%) of your earnings to your nominated super fund. While this might seem like a lot, depending on your ideal cost of living in retirement, you may wish to contribute additional money to boost your savings. One way of doing this is through salary sacrificing.

Salary sacrificing is where you establish an arrangement with your employer to pay a portion of your pre-tax salary to your super account as a concessional contribution. There are a few benefits to this:

- Boost to your overall contributions to your super fund

- Reduce your taxable income, therefore, paying less tax

- Works as a forced saving so you don’t need to worry about putting money away to contribute later

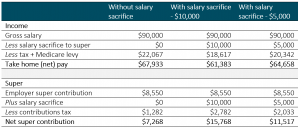

To show you how this could work for you, here’s an example for someone earning $90,000 p.a.:

The above example shows how your after-tax pay would be affected if you salary sacrificed $10,000 in one year, the difference is $6,550 per year or $126 per week. If this looks too much for your circumstance, perhaps consider reducing your super contributions to $5,000. Now your take-home pay is $64,658, therefore an after-tax reduction of $3,275 per year or $63 per week.

Salary sacrificing is a great tool to help boost your super savings, however, there can be some traps for young players. Be sure to speak with your financial adviser to establish how salary sacrificing can best work for you.

Please note this article provides general advice and has not taken your personal or financial circumstances into consideration. If you would like more tailored superannuation or financial advice, please contact us today. One of our advisers would be delighted to speak with you.